Improving the Online Shopping Experience:

The Role of Embedded Finance in Boosting Conversion Rates - A Report

January 23, 2023

The Role of Embedded Finance in Boosting Conversion Rates - A Report

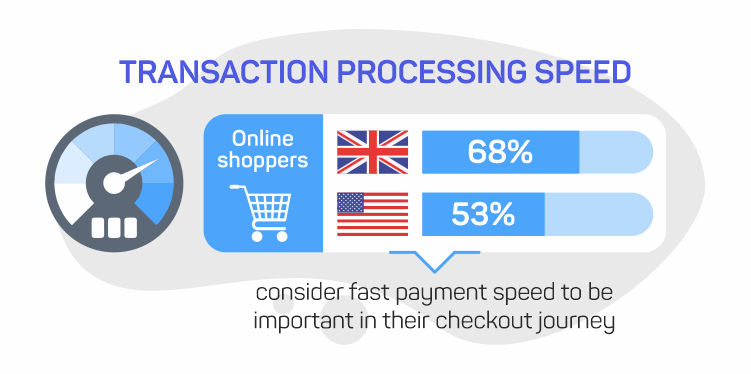

This figure was lower in the United States, but the majority of those surveyed (53%) still considered fast payment clearing speeds to be important. It is also notable that U.S. respondents were particularly irked when websites failed to update quickly. A webpage not loading on the first attempt was seen as more annoying than any other event in the survey by participants in the United States.

In short, our survey found that faster payment speeds greatly improve the customer experience, while significantly reducing the possibility that consumers will abandon purchases. The faster checkout speeds associated with embedded finance have already proved popular, with a recent study from Temenos discovering that 60% of UK consumers have used embedded finance products during the checkout process in the last 12 months.[5]

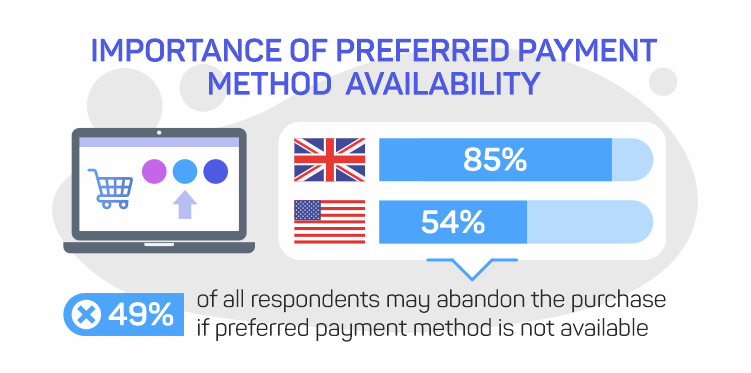

There was also agreement on the negative side of this factor. Roughly half of all respondents from both countries (49%) stated that they would certainly or probably abandon purchases if their preferred payment method was not available. In the UK, the lack of availability of a preferred payment method was listed as the second most negative experience among participants. Younger people also tended to view the availability of the preferred payment method as a bit more important for positive shopping experiences than older people (rho=-.140).

Businesses offering embedded finance features would therefore be advised to ensure that they offer as many payment methods as possible. Embedded payment methods, such as SmartPay Rewards, will also become increasingly important, which will need to be factored in vendor processes.

It is hard to quantify precisely why there was this contrast in attitudes. But perhaps the much larger geographical area associated with the United States could play some role in the estimation of insurance, as delivery simply becomes more logistically complex. However, it is notable that additional embedded solutions were at least appreciated in both countries, even if they are seen as being very much more worthwhile by U.S. consumers.

We can reasonably expect the prevalence of these figures to grow as embedded payments become a more prominent innovation, and such services can only be delivered via embedded technology.

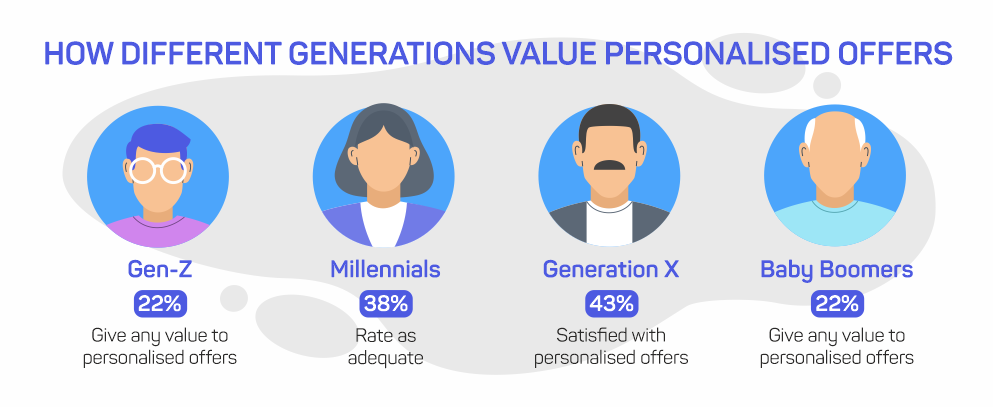

Demographics were also particularly important in this area. Respondents from ‘Generation X’ were by far the most satisfied with personal offers, with 43% of this group stating that they were adequate most or all of the time. ‘Millennials’ offered a similar response rate (38%), but this contrasted with older and younger participants. Both ‘Gen-Z’ and ‘Baby Boomer’ participants rated the offers that they received much less favourably, with only 22% of these groups indicating that they were adequate most or all of the time.

Personalised offers can therefore be viewed as icing on the embedded finance cake; not an essential feature, but one that is certainly appreciated, and especially by ‘Generation X’. It seems that personalised offers are currently designed with certain demographics in mind, and that there is potential for other groups to be more effectively targeted.

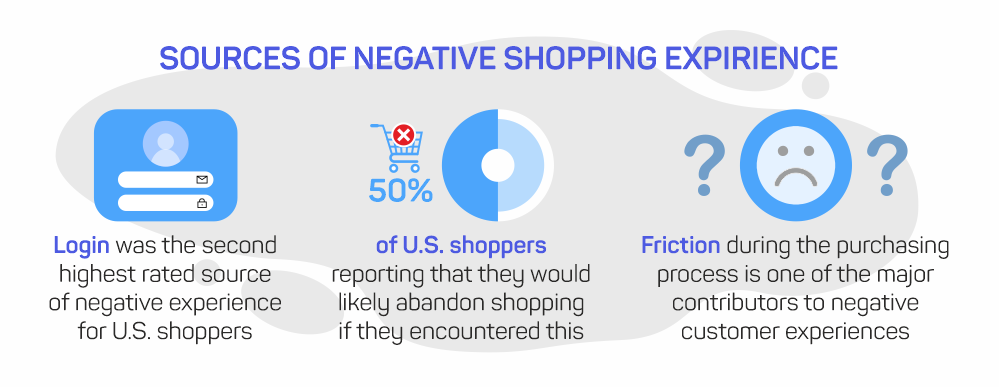

Creating friction for consumers can therefore cause businesses major problems, and lead to a significant tranche of squandered revenue.

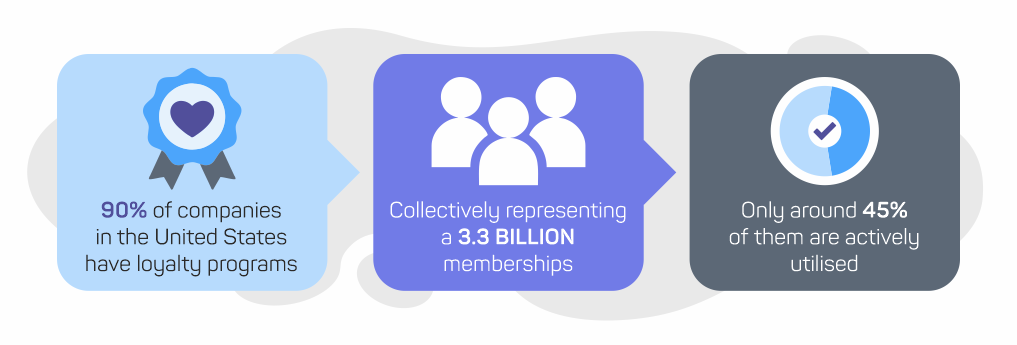

This means that loyalty programs can play a significant role in not only delivering a positive consumer experience, but also in retaining customers over an extended period of time. However, the prevalence of loyalty programs means that they can be taken for granted, or else companies need to offer something outstanding in order to really obtain customer loyalty.

In accordance with this, our survey generally found that loyalty rewards are associated with positive customer experiences. But their absence is not really regarded as a particular negative. This was consistent across respondents from both the United States and the UK.

In Britain, loyalty reward programmes were only rated as being of moderate importance for a positive shopping experience. Only 29% of respondents considered it either the most important factor, or very important in their overall shopping experience. This differs somewhat with the United States, with participants in the survey based in the US considering loyalty rewards to be the third most important feature of a positive shopping experience.

However, there was stronger correlation on whether or not the existence of a loyalty programme was a significant negative. Relatively few consumers from either the United States or the UK would abandon a purchase due to the absence of a loyalty programme.

Nonetheless, this is clearly another area where businesses can set themselves aside from the competition by offering attractive rewards, and, in the process, achieving loyalty among consumers. And it should be emphasised that embedded finance is the ideal solution to deliver this functionality.